The FinTech App Reality Check: What It Actually Takes to Ship in 2026

Building FinTech Apps in 2026: Compliance, Speed, and What Actually Ships looks very different from what it did just a few years ago. Here's what you need to know right now:

The short answer:

- Compliance is no longer a post-launch checkbox — it's baked into the architecture from day one

- MVPs now take 8–16 weeks with modern AI-assisted engineering (down from 6+ months)

- Budget range: $40,000–$150,000 for an MVP, depending on complexity and compliance scope

- The leading cause of FinTech startup failure isn't bad code — it's compliance gaps (78% of failures)

- Progressive Web Apps (PWAs) now handle most FinTech use cases, cutting App Store friction and fees

- BaaS providers like Stripe Treasury and Unit let startups skip the multi-year banking license process

A few years ago, building a FinTech product felt like a sprint. Ship fast. Scale quickly. Sort out compliance later. That mindset is now a liability.

FinTech has quietly become infrastructure. Millions of people use instant payments, AI-driven credit decisions, and API-connected bank accounts every single day. When your app is part of someone's ability to pay rent or make payroll, the tolerance for error drops to zero.

Regulators noticed. And they responded. Global AML and KYC penalties hit $4.5 billion in 2024. The Synapse bankruptcy froze $160 million in customer funds, taking down startups that had perfectly good code but dangerously fragile compliance foundations. Meanwhile, deepfake-based identity fraud attempts surged over 1,100% since early 2025.

The math is simple: the cost of retrofitting compliance after launch is 3 to 5 times higher than building it in from the start. The companies winning in 2026 aren't the ones moving fastest — they're the ones moving deliberately, with compliance embedded into every sprint, every deployment, and every infrastructure decision.

This guide breaks down exactly how to do that.

Why Compliance is the New Speed in 2026 FinTech Development

In the early 2020s, the mantra was "move fast and break things." In 2026, if you break the ledger, you break the business. We’ve seen a massive paradigm shift where regulation now shapes the product from day one. This isn't just because we like paperwork; it's because the complexity of modern finance—instant payments via FedNow, AI-driven lending, and open banking—requires safeguards at scale.

If you treat compliance as a hurdle, you’ll lose. If you treat it as a feature, you’ll win. Why? Because trust is the only currency that matters in FinTech. A beautiful UI is useless if a user's funds are frozen due to a KYC (Know Your Customer) failure.

Today, every successful app must navigate a complex web of frameworks:

- SOC 2 Type II: The baseline for security and data privacy.

- PCI-DSS v4.0: Now fully enforced, requiring more rigorous authentication and monitoring for anything touching card data.

- GDPR & CCPA: Non-negotiable for data residency and user "right to be forgotten."

- KYC/AML Orchestration: Moving beyond simple ID uploads to real-time risk scoring.

As we noted in The Compliance Cliff: Why 2025’s Apps Failed and How to Build for 2026 Regulations, many founders who deferred these audits until post-launch found themselves facing catastrophic rebuild costs. To avoid this, we recommend How to Build a Compliance Engine for Fintech: KYC Orchestration, AML Pipeline & RegTech Architecture to ensure your engine is audit-ready from the first line of code.

FinTech in 2026: It's Not About Moving Fast Anymore because the "fast" teams are often the ones getting shut down by regulators.

Building FinTech Apps in 2026: Compliance, Speed, and What Actually Ships with DevOps

The secret to shipping fast without breaking the law is "Compliance as Code." By integrating automated compliance checks directly into your CI/CD pipelines, we ensure that every deployment is pre-validated against regulatory requirements.

Using Infrastructure as Code (IaC) tools like Terraform or Pulumi allows us to define your entire environment—from database encryption to firewall rules—as versioned, auditable code. This means if an auditor asks how your data was secured on a random Tuesday six months ago, we can show them the exact code state.

DevSecOps isn't just a buzzword in 2026; it’s a survival mechanism. Mature DevSecOps teams in finance have automated 63% of their governance, leading to a 50% reduction in vulnerabilities. For more on how we implement these frameworks, check out our FinTech development services.

AI-Powered Compliance and Fraud Detection

AI has moved from a "nice-to-have" chatbot to the core of the compliance engine. In 2026, we use "Agentic AI"—autonomous systems that don't just flag issues but actively investigate them.

- Real-time Fraud Detection: AI models now analyze behavioral patterns (how a user holds their phone, typing speed) to catch account takeovers before a transaction even occurs.

- Automated KYC: Document extraction is now 99.9% accurate, reducing onboarding times from days to seconds.

- Predictive Compliance: AI can now scan upcoming regulatory changes and flag gaps in your current architecture before they become legal issues.

You might wonder How Do Fintech Apps Stay Compliant and Deliver ROI in 2026? The answer is automation. By reducing false positives in AML (Anti-Money Laundering) checks—which used to be as high as 90%—we save our clients millions in operational spend. This cross-pollination of tech is something we’ve mastered, as seen in From Fintech To Healthcare: How Multi-Industry App Developers Solve Complex Problems.

The 2026 Tech Stack: Balancing Performance and Security

Choosing the right tech stack for Building FinTech Apps in 2026: Compliance, Speed, and What Actually Ships is about choosing "boring" stability for the data and "cutting-edge" speed for the interface.

The Backend: Node.js and GoFor high-concurrency financial transactions, Go (Golang) has become the gold standard due to its efficiency and safety. Node.js remains a favorite for rapid API development, especially when paired with TypeScript to prevent the types of "undefined" errors that lose money.

The Database: PostgreSQLWhile NoSQL has its place, the core of your FinTech app belongs in PostgreSQL. It is strictly ACID-compliant, ensuring that if a transaction fails halfway through, the database rolls back to a safe state. We use Row-Level Security (RLS) to ensure multi-tenant data isolation—a must for any SaaS-based financial tool.

Cloud-Native and Disaster RecoveryIn 2026, "the cloud" means more than just AWS or Azure. It means a multi-region, disaster-recovery-ready architecture. If an entire AWS region goes dark, your users still need to pay for their coffee. We architect for 99.99% availability using container orchestration and automated failover.

For a deeper dive into the technical roadmap, see How to Build a Fintech App in 2026: A Step-by-Step Guide. And remember, scaling isn't just about handling more users; it's about doing it securely. We discuss this in From MVP to Global Scale: Navigating the Security Gap.

PWA vs Native: Building FinTech Apps in 2026: Compliance, Speed, and What Actually Ships for Mobile

One of the biggest debates in 2026 is whether you actually need a native iOS or Android app. For many FinTech products, the answer is now "No."

Progressive Web Apps (PWAs) have matured significantly. Thanks to WebAuthn, PWAs can now access FaceID and TouchID directly through the browser. This allows for biometric security without the 30% "Apple Tax" or the 7-day delay for App Store compliance patches.

When to go Native:

- If you need high-performance NFC (for "tap to pay" features).

- If your app requires deep background processing.

- If you are building a high-frequency trading platform where every millisecond of UI latency matters.

When to go PWA:

- For neobanks, budgeting tools, and lending platforms.

- When you need to push critical compliance updates instantly to all users.

- When you want to bypass the friction of an app store download to increase conversion.

We outline the decision matrix in our Mobile App Development Process In 2026: Ultimate Step-by-Step Guide. For many, the "PWA-first" approach is becoming the standard for The New Rules of Fintech App Development in 2026.

Measuring Success: DORA Metrics and Building FinTech Apps in 2026: Compliance, Speed, and What Actually Ships

How do you know if your engineering team is actually good, or just busy? In 2026, we use DORA metrics to measure DevOps maturity and compliance effectiveness. If you are hiring a partner, these are the numbers you should demand.

- Deployment Frequency: How often do you ship code? High-performing FinTech teams ship multiple times a day.

- Lead Time for Changes: How long does it take from "code committed" to "code in production"? In a compliant environment, this includes automated testing and security gates.

- Mean Time to Recovery (MTTR): When (not if) something goes wrong, how fast can you fix it? High performers recover 2,600x faster than low performers.

- Change Failure Rate: What percentage of your deployments cause a failure? In FinTech, this needs to be near zero.

At Bolder Apps, we believe you shouldn't just "buy hours." You should buy velocity and reliability. We explain why in Don't Buy Hours, Buy Velocity: 5 DORA Metrics You Must Demand.

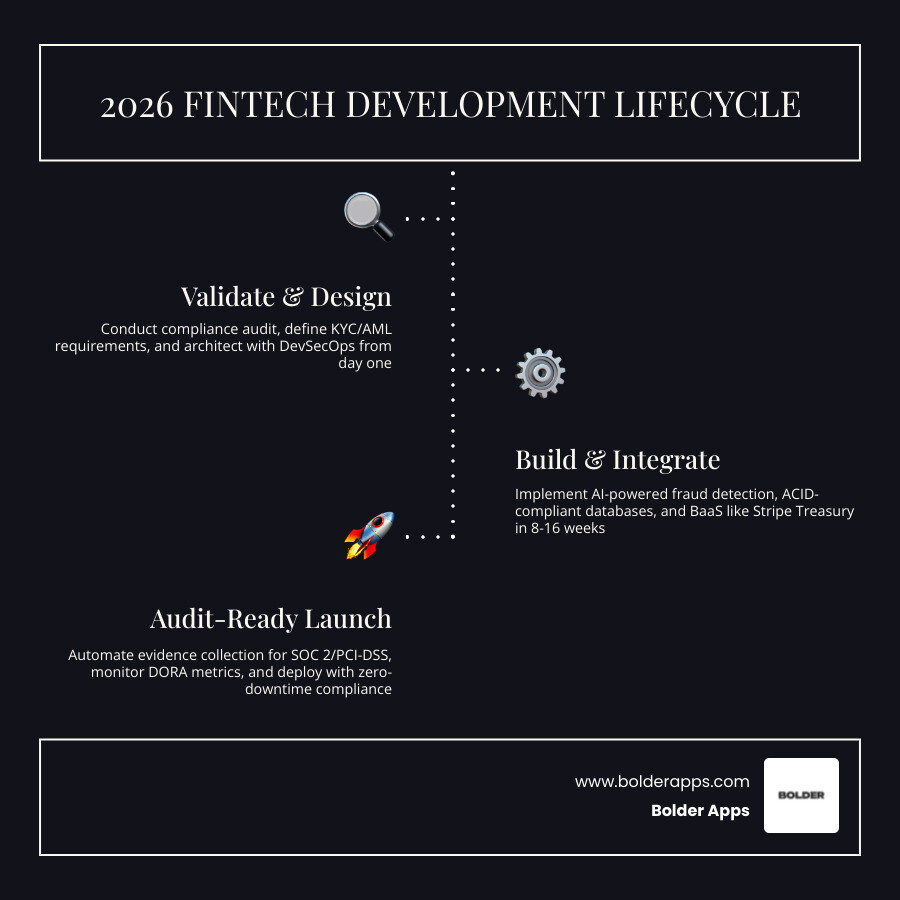

Realistic Costs, Timelines, and the Roadmap to Launch

Building a FinTech app isn't cheap, but it’s more accessible than it used to be thanks to Banking-as-a-Service (BaaS) providers.

The MVP Budget ($40,000 – $150,000)

A basic payment app or budgeting tool can be launched for around $40k-$80k. A more complex neobank or lending platform with custom risk engines will push toward the $150k+ mark. Why the range? It comes down to Compliance Scope. If you are handling the money movement yourself, you need more licenses and more security audits than if you are just a "skin" on top of a partner bank.

For a full breakdown, see How Much Does It Cost To Make An App In 2026: Full Breakdown.

The 8–16 Week Timeline

With AI-assisted coding and pre-built integrations like Stripe Treasury or Unit, we can get an MVP to market in under 4 months.

- Weeks 1-2: Discovery and Regulatory Mapping. (Don't skip this!)

- Weeks 3-10: Core Development and BaaS Integration.

- Weeks 11-14: Security Audits and Penetration Testing.

- Weeks 15-16: Compliant Launch.

Monetization Models

How will you make money? In 2026, the most successful apps use a hybrid model:

- Interchange Fees: Earning a small percentage every time a user swipes a card.

- Subscription Tiers: Charging for premium features like metal cards or advanced analytics.

- Assets Under Management (AUM): Common for investment apps.

- Interest Arbitrage: The classic banking model, modernized.

For more details on the launch sequence, refer back to How to Build a Fintech App in 2026: A Step-by-Step Guide.

Frequently Asked Questions about 2026 FinTech Development

Why has compliance replaced 'move fast and break things' in 2026?

Because the stakes are higher. In 2026, FinTech is infrastructure. Regulators have moved from reactive to proactive, using automated enforcement tools. If your app fails a compliance check, your partner bank can shut down your API access in milliseconds. Trust is now your most expensive asset; breaking things costs too much to be a viable strategy.

What is the average cost of a FinTech MVP in 2026?

You should expect to invest between $40,000 and $150,000. The lower end covers apps that leverage BaaS providers to handle the heavy regulatory lifting. The higher end is for products requiring custom blockchain integrations, complex AI underwriting, or multi-state lending licenses.

When should a FinTech app choose PWA over Native?

Choose a PWA if you want to launch quickly, avoid App Store fees, and need to push security updates instantly. It’s perfect for 90% of FinTech use cases like budgeting, simple banking, and insurance. Choose Native only if you need advanced hardware access (NFC) or if your brand relies on being in the App Store for "prestige" discovery.

Future-Proofing Your Financial Product

Building a FinTech app in 2026 is a balancing act. You need the speed to beat your competitors to market, but the architectural rigor to ensure you aren't shut down by an auditor six months later.

At Bolder Apps, we’ve been navigating this landscape since 2019. We were recently named the top software and app development agency in 2026 by DesignRush, a recognition of our commitment to shipping products that aren't just beautiful, but are "load-bearing" and compliant. You can verify these details on bolderapps.com.

Our USP is simple: we combine US-based leadership (with a dedicated in-shore CTO for every project) with senior distributed engineers. This means you get strategic, data-driven creation without any "junior learning on your dime." We operate on a fixed-budget model with milestone-based payments, giving you the certainty you need to manage your runway effectively.

Whether you are in Miami or operating globally, our team is ready to help you map your regulatory surface area and build a product that actually ships—and stays shipped.

Ready to build the future of finance?

Let’s build something bold (and compliant) together.